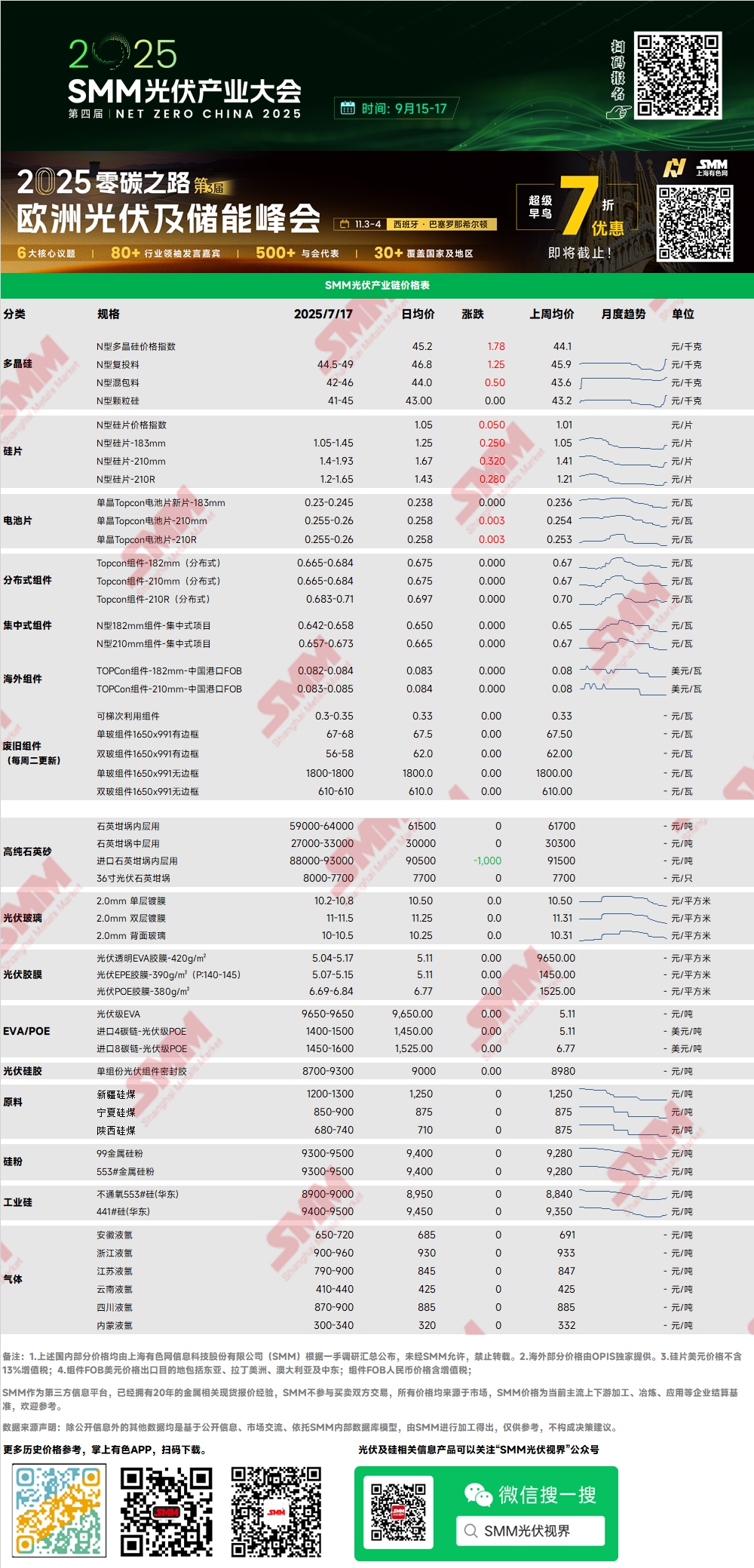

Polysilicon: This week, the price index for N-type polysilicon was 45.23 yuan/kg. The quotations for N-type recharging polysilicon ranged from 44.5-49 yuan/kg, while those for granular polysilicon ranged from 41-45 yuan/kg. Polysilicon quotations rose slightly. Early in the week, market quotations gradually stabilized, but subsequently, with a significant jump in the new round of wafer quotations and the cost calculation basis reaching a comprehensive price of 43.87 yuan/kg, some rod-shaped polysilicon enterprises were supported to continue raising their quotations. However, it should be noted that there have been no direct new orders for the high-priced segment yet, with some orders being shipped with a mix of new and old goods. The market continues to focus on mainstream transactions.

Wafer: This week, the price for N-type 183 wafers was 1.05-1.45 yuan/piece, with 210R wafers quoted at 1.2-1.65 yuan/piece and 210mm wafers at 1.4-1.93 yuan/piece. Wafer quotations were significantly raised this week. A self-discipline meeting related to the wafer enterprise industry was held this week, and wafer enterprises also began to quote based on full costs. Some top-tier enterprises significantly raised their quotations, while others cautiously observed the market, resulting in a fragmented market quotation landscape. Currently, there have been no actual transactions for the voluntarily high-priced segment, and the market is observing downstream acceptance and price adjustments.

Cell: For P-type cells, the price for high-efficiency PERC182 solar cells was 0.265-0.27 yuan/W, with export orders. The market operating rate was extremely low, and producers started or stopped production lines based on orders. For N-type cells, firstly, for TOPCon high-efficiency solar cells, the transaction range for 183N was 0.22-0.23 yuan/W, for 210RN it was 0.24-0.25 yuan/W, and for 210N it was also 0.24-0.25 yuan/W. Secondly, for HJT solar cells, the mainstream quotation for HJT30% silver-clad copper (with 25% or higher efficiency) was 0.35-0.36 yuan/W. Planned production for July decreased, with market demand possibly weakening and prices under pressure.

Driven by price increases at individual solar cell plants yesterday, today multiple producers initiated a strategy of following the price rise: The highest quotation for TOPCon183N was raised to 0.25 yuan/W, with 210N/210RN reaching a maximum of 0.265 yuan/W. According to the SMM survey, some solar cell plants had already proactively slowed down their shipping rhythm early this week. Firstly, they were observing the upward trend in wafer prices. If they maintained the original shipping rhythm, they might face the risk of purchasing at high prices, aiming to avoid potential cost pressures. Secondly, they were conserving strength for price recovery, responding to the call of the industry chain's anti-"rat race" competition spirit, and simultaneously reversing the situation of continuous sales losses. Currently, multiple solar cell plants have strengthened their bargaining power by suspending shipments or delaying outflows from warehouses.

PV Module: This week, quotations for PV modules rose, with distributed quotations increasing by 2 fen/W, reaching a maximum price of 0.7 yuan/W. The price increase was mainly driven by anti-"rat race" competition policies, with upstream raw material prices rising and module costs increasing significantly. However, the acceptance of downstream module clients was limited, especially for centralized clients, where project yields faced significant challenges. A large number of projects might be delayed. For the distributed demand side, demand in the second half of the year would shrink significantly.

PV Glass: This week, the quotation center for PV glass enterprises shifted downward by 5. As of now, the mainstream quotation for 2.0mm single-layer coated PV glass in China was 10.0 yuan/m². The mainstream quotation for 3.2mm single-layer coated PV glass was 17.0 yuan/m², and for 2.0mm back glass it was 10.3 yuan/m². This week, the transaction center for domestic PV glass shifted downward. Influenced by the accelerated pace of production cuts on the supply side in July, downstream module enterprises in China began to stock up and purchase, with market transaction enthusiasm recovering somewhat. Although the overall supply and demand situation showed a supply surplus, the addition of stockpiling volumes halted the rise in glass inventory. It is expected that during the settlement period after July, the glass inventory level would decline, and with leading enterprises still planning production cuts, the supply side would face insufficient supply in the future, and enterprises' stockpiling mentality would continue to increase.

High-Purity Quartz Sand: This week, quotations for domestic high-purity quartz sand fell. Current market quotations are as follows: 59,000-64,000 yuan/mt for inner-layer sand, 27,000-33,000 yuan/mt for middle-layer sand, and 17,000-22,000 yuan/mt for outer-layer sand. This week, quotations from domestic high-purity quartz sand enterprises decreased, but the speed of price decreases slowed down. Overall, the planned production for wafers remained low recently, with limited demand for quartz sand. Meanwhile, some sand enterprises had increased their operating rates earlier, resulting in a relatively large market supply volume. Sand enterprises still expected inventory backlogs. However, with the recent upward trend in wafer prices, sand enterprises' willingness to reduce prices and destock had narrowed. It is expected that the market would enter a bargaining phase recently. Although sand prices are still in a downward cycle overall, the extent of the decrease is expected to narrow significantly.

EVA: This week, the price of PV-grade EVA ranged from 9,500-9,750 yuan/mt. Recently, film enterprises have been replenishing their stocks, and petrochemical plants have been gradually destocking. Some petrochemical enterprises on the supply side have switched to producing non-PV materials, and some petrochemical plants are still in their maintenance cycles. The supply of PV materials continues to tighten. On the demand side, module planned production in July fell short of expectations, and the overall operating rate of film enterprises was low. The market as a whole showed a weak supply and demand situation. It is expected that PV material prices would remain in the doldrums in the near future.

Film: The mainstream price range for EVA film is 12,000-12,300 yuan/mt, and for EPE film it is 13,000-13,200 yuan/mt. On the demand side, module planned production declined in July, with weak demand. On the cost side, the price of PV-grade EVA remained low, providing cost support for film prices. Under the dual squeeze of cost and demand, film prices remained in the doldrums.

POE: The domestic delivery-to-factory price for POE ranges from 11,000-14,000 yuan/mt, with some transactions occurring recently. On the demand side, module planned production declined, and the operating rate of film enterprises decreased, with demand falling short of expectations. It is difficult for prices to rise. It is expected that POE PV material prices would remain weak and stable in the near future.

Terminal:

Key bid-winning information during the statistical period from July 7, 2025 to July 11, 2025:

1. In the section titled "Publication of Bid Evaluation Results for the 2025 Annual Framework Purchase of PV Modules by China Railway Construction Network Information Technology Co., Ltd.", LONGi Solar Technology Co., Ltd., Jinko Solar Co., Ltd., TrinaSolar Co., Ltd., Tongwei Co., Ltd., Hefei JA Solar Technology Co., Ltd., Chint New Energy Technology Co., Ltd., Yingli Energy Development Co., Ltd., GCL SI Technology Co., Ltd., DAS solar New Energy Technology Co., Ltd., and Changshu Canadian Solar Power Technology Co., Ltd. jointly won the bid for PV modules with a total capacity of 3000MW. The specific prices have not yet been disclosed.

2. Zichuang Guangke Green Energy (Shenzhen) Engineering Co., Ltd. won the bid for 7,954 PV modules of the Zichuang Guangke brand at a price of 2.8833 million yuan, with a total bid-winning capacity of 4.6132MW. The project name is "Publication of Bid-winning for Monocrystalline Silicon PV Module Purchase in the 10kV Transmission Project for Distributed PV at Phase I of the Ningde City Land-Water Combined Transport Center".

3. In the "Publication of Bid-winning Candidates for Equipment and Material Procurement for the Nonguang Complementary PV Power Generation Project in Daliang Town, Rong'an County, Liuzhou (KLLZG251001) (Secondary Tender for Bid Package 1 and Bid Package 3)", Chint New Energy Technology Co., Ltd. won the bid for PV modules with a capacity of 42.939MW at an average price of 0.72 yuan/W.

》View the SMM PV Industry Chain Database

![[SMM PV News] Armenia Hits 1.1 GW Solar Capacity,](https://imgqn.smm.cn/usercenter/qQwIB20251217171741.jpg)

![Spot Market and Domestic Inventory Brief Review (February 5, 2026) [SMM Silver Market Weekly Review]](https://imgqn.smm.cn/usercenter/tSwaX20251217171735.jpg)